Rushmore Servicing: A Clear Guide to Mortgage Payments, Account Management, and Borrower Support

Rushmore Servicing is a mortgage servicing company that helps homeowners manage their accounts after their loans are transferred, assigned, or placed under a new servicing platform. For borrowers, Rushmore’s name appears when they receive notice that their mortgage payments, escrow details, and account communication will be handled by Rushmore. This change can be confusing since most homeowners choose a lender, not necessarily the company that later services the loan. The lender provides funds; the servicer manages the account after activation. Rushmore may handle payments, online access, payoff requests, escrow questions, tax and insurance information, customer service, and borrower assistance. Understanding this process helps homeowners avoid missed payments, late fees, confusion, and stress when managing their home loans.

What Is Rushmore Servicing?

Rushmore Servicing is best understood as a mortgage servicing platform that helps manage active mortgage accounts. When a borrower’s loan is serviced by Rushmore, the company may be responsible for collecting payments, sending mortgage statements, providing account information, and helping borrowers understand their loan status. Mortgage servicing can include many day-to-day responsibilities that continue long after the loan closes. These responsibilities may involve posting monthly payments, maintaining escrow accounts, issuing annual tax statements, updating insurance information, answering borrower questions, and helping customers navigate hardship or loss-mitigation options when available. For homeowners, the most important point is that Rushmore Servicing is not simply a name on a statement; it is the company or servicing brand borrowers may need to contact for payment and account-related matters. If a borrower receives a valid servicing transfer notice, they should carefully read it, confirm the effective date, check where future payments should be sent, and create online access if available.

Why Borrowers Search for Rushmore Servicing

Many people search for Rushmore Servicing after receiving a mortgage transfer notice, seeing the name on a billing statement, or needing to log in to make a payment. Mortgage servicing transfers are common, but they can make borrowers nervous, even though the terms usually stay the same. Borrowers may wonder about the legitimacy of the transfer, changes to payments, escrow handling, or automatic payment updates. Others search for the customer service number, access to the portal, help with late payments, or clarification of a letter. These searches come from practical concerns, not curiosity. Homeowners want clear answers, as mortgage accounts are serious responsibilities, and small mistakes in timing, setup, or communication can cause problems.

How Mortgage Servicing Works

Mortgage servicing is the management of a loan after closing. This includes handling payments, account records, escrow fund disbursement, notices, and borrower support. After a home loan begins, it may be sold or transferred to another servicer, but this does not change the borrower’s interest rate, loan balance, maturity date, or original agreement. Most often, only the servicer changes, not the core contract. The servicer must manage the account in accordance with the loan documents and rules. For Rushmore Servicing customers, Rushmore becomes the primary contact for payments, records, notices, and support. Homeowners should keep transfer notices, payment confirmations, escrow statements, and customer service communications. Careful recordkeeping during a servicing transfer ensures borrowers can prove when and where payments were sent and what instructions they received.

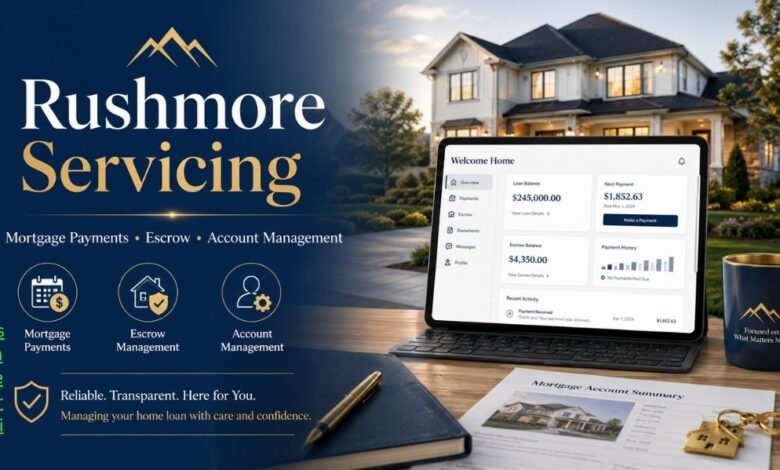

Rushmore Servicing Account Access

A major part of modern mortgage management is online account access. Borrowers typically want a secure portal to view their loan balance, payment due date, recent transactions, escrow activity, documents, and correspondence. Rushmore Servicing provides digital account tools that may allow borrowers to manage their mortgages more conveniently. Online access can be useful because it reduces the need to wait for paper mail or to call customer service for basic questions. Through an account portal or mobile app, borrowers can make payments, set up AutoPay, view statements, download documents, and check account messages. However, homeowners should always ensure they use the official platform and avoid fake websites or suspicious links. Mortgage scams can target borrowers during transfers, so it is smart to verify login pages, avoid clicking links in unknown emails, and compare any payment instructions with official transfer notices.

Payments and AutoPay

Timely mortgage payments are a borrower’s key responsibility. Rushmore Servicing offers payment options online, by phone, mail, or automatic payment, depending on account availability. Setting up AutoPay carefully can reduce the risk of missing payments. Confirm the withdrawal date, payment amount, and bank account details, and be aware of any possible escrow changes. When loans transfer, do not assume previous automatic payments continue; cancel or update any prior payment arrangements and set up new ones with the current servicer. Monitor bank activity and mortgage account history during transitions. Payments sent to the wrong servicer or posted late can cause stress, even if you acted in good faith.

Escrow, Taxes, and Insurance

Many mortgage accounts include an escrow account, which is used to collect money for property taxes, homeowners insurance, and sometimes other required items. If Rushmore Servicing manages a borrower’s escrow account, it may collect part of the monthly payment and later use those funds to pay tax bills or insurance premiums when due. Escrow can be confusing because monthly payments may change after an annual escrow analysis. A borrower may see a higher payment if taxes or insurance costs increase, or if there is an escrow shortage. A lower payment may happen if costs decrease or if the account has an overage. Homeowners should read escrow statements carefully and compare them with local tax bills and insurance notices. If something looks wrong, such as duplicate insurance, missing tax payments, or an unexpected shortage, the borrower should contact customer service quickly and keep written records of the issue.

Customer Service and Borrower Support

Customer service is an important part of any mortgage servicing experience. Borrowers may contact Rushmore Servicing for questions about payments, statements, online access, escrow, payoff amounts, insurance documents, tax forms, or account transfers. Some borrowers may also need help because of financial hardship, job loss, medical issues, divorce, disaster damage, or other serious life events. In those cases, the servicer may provide information about available options, which could include repayment plans, forbearance, loan modification review, or other assistance programs depending on the loan type and investor rules. Borrowers should not wait until the situation becomes severe. Early communication can make a major difference. When contacting customer service, homeowners should write down the date, time, representative name if provided, and summary of the conversation. If documents are submitted, borrowers should keep copies and confirm receipt.

What to Do After a Servicing Transfer

If your mortgage has been transferred to Rushmore Servicing, the first step is to read the official transfer notice carefully. The notice should explain when the transfer takes effect, where future payments should be sent, and how to contact the new servicer. Borrowers should update payment methods, set up online access, review the first statement, and confirm that the loan balance and payment amount appear correct. It is also smart to check whether the escrow information was transferred properly. During the first one or two billing cycles after a transfer, borrowers should be extra careful. They should save payment confirmations, monitor their bank account, and check that payments are posted correctly. If something does not match, contact the servicer quickly. A servicing transfer should not change the borrower’s core loan terms, but administrative errors can happen, so careful review is always helpful.

Common Concerns About Rushmore Servicing

Borrowers may have several concerns when dealing with Rushmore Servicing or any mortgage servicer. Common concerns include payment posting delays, escrow changes, difficulty accessing an online account, confusing notices, insurance tracking issues, or trouble reaching customer service. Some borrowers may also worry about whether their loan is still owned by the same investor or whether the servicer has the authority to collect payments. These concerns are understandable, as mortgage servicing involves significant financial obligations and important legal rights. The best response is to stay organized, communicate in writing when possible, and request clarification when something is unclear. Borrowers should never ignore letters from their mortgage servicer, even if they believe the information is wrong. Instead, they should respond promptly, provide documentation, and ask for written confirmation when issues are corrected.

Complaints and Problem Resolution

If a borrower cannot resolve an issue directly through customer service, they may need to file a formal complaint or written dispute. Rushmore Servicing provides complaint-related contact options, and borrowers can usually submit written concerns about payment errors, escrow problems, account inaccuracies, or servicing issues. A strong complaint should include the borrower’s name, loan number, property address, a clear explanation of the problem, dates, payment details, and copies of supporting documents. The tone should be professional and factual. Borrowers should avoid vague complaints and instead explain exactly what happened and what correction they are requesting. If the issue remains unresolved, homeowners may also consider contacting a housing counselor, legal professional, or appropriate consumer protection agency. Mortgage problems can become serious quickly, so written documentation is one of the strongest tools a borrower has.

Safety Tips for Borrowers

Because mortgage accounts involve sensitive information, borrowers should protect themselves from scams. Anyone using Rushmore Servicing should confirm payment instructions through official notices or verified customer service channels. Be cautious with emails, text messages, or phone calls that demand immediate payment, ask for unusual payment methods, or threaten sudden foreclosure without proper documentation. Borrowers should never share full Social Security numbers, bank login details, or passwords with unknown callers. A real mortgage servicer may require identity verification, but borrowers should contact them through trusted channels when unsure. It is also helpful to use strong passwords, enable security features when available, and review account activity regularly. Mortgage fraud can happen when borrowers are confused after servicing transfers, so caution is important.

Is Rushmore Servicing Important for Homeowners?

Yes, Rushmore Servicing can be very important for homeowners whose mortgage accounts are handled through the platform. Even though a servicer may not be the original lender, it plays a major role in the borrower’s monthly mortgage experience. The servicer affects how payments are made, how statements are received, how escrow is managed, and how account questions are answered. A borrower who understands the servicing process is more likely to avoid confusion and respond quickly when something changes. The key is not to panic when a servicing transfer happens, but also not to ignore it. Homeowners should verify the transfer, update payment information, keep records, and communicate early when problems appear.

Conclusion

Rushmore Servicing is a mortgage servicing platform that helps manage home loan accounts, payments, statements, escrow matters, documents, and borrower support. For homeowners, the name often becomes important after a servicing transfer or when they need to access their mortgage account online. The most important thing borrowers can do is stay informed, keep records, verify payment instructions, and communicate quickly if something looks wrong. Mortgage servicing can feel complicated, but it becomes easier when borrowers understand the difference between a lender and a servicer, review their statements carefully, and use official account tools responsibly. Whether someone is making a regular payment, setting up AutoPay, checking escrow, or resolving a complaint, a careful and organized approach can help protect their home loan account and reduce unnecessary stress.

(FAQs)

What is Rushmore Servicing?

Rushmore Servicing is a mortgage servicer, which means it may handle ongoing mortgage account management, including payments, statements, escrow information, customer support, payoff requests, and borrower assistance. A mortgage servicer is not always the same company that originally gave the loan.

Why did my mortgage transfer to Rushmore Servicing?

Mortgage loans are often transferred from one servicer to another. If your account is transferred to Rushmore Servicing, you should receive an official notice with the transfer date, new payment instructions, and contact details. The transfer usually does not change your original loan terms.

Does Rushmore Servicing change my mortgage payment?

A servicing transfer itself usually does not change your loan terms. However, your monthly payment may still change due to escrow adjustments, insurance changes, tax increases, interest rate changes on adjustable-rate loans, or other account-related updates.

How can I make a payment to Rushmore Servicing?

Borrowers may be able to make payments through online account access, mail, phone, or automatic payment options, depending on their account setup. Always use the official payment instructions provided in your servicing notice or account statement.

Should I set up AutoPay again after my loan transfers?

Yes, you should check this carefully. Old automatic payments may not always continue after a servicing transfer. Confirm whether your previous AutoPay was canceled and set up a new payment method with Rushmore Servicing if needed.

What should I do if my payment is not showing?

First, check your bank account and payment confirmation. Then contact Rushmore Servicing customer support with the payment date, amount, confirmation number, and method used. Keep written records until the issue is fixed.

What is an escrow account?

An escrow account is used to collect funds for property taxes, homeowners’ insurance, and, in some cases, other required costs. Your mortgage servicer may collect escrow funds as part of your monthly payment and use them to pay bills when due.

Why did my escrow payment increase?

Your escrow payment may increase if property taxes, insurance premiums, or escrow shortages go up. Mortgage servicers usually review escrow accounts yearly and adjust the monthly payment based on expected future costs.

Can Rushmore Servicing help if I cannot pay my mortgage?

If you are facing financial hardship, contact Rushmore Servicing as early as possible. Depending on your loan type and situation, there may be assistance options such as repayment plans, forbearance review, or loan modification review.

What should I do if I receive a suspicious mortgage call or email?

Do not share sensitive information with unknown callers or suspicious links. Verify the message through official account statements, trusted contact channels, or your secure borrower portal. Mortgage scams are common during servicing transfers.

Can I request a payoff statement from Rushmore Servicing?

Yes, borrowers can usually request a payoff statement from their mortgage servicer. This statement shows the amount needed to fully pay off the mortgage by a specific date, including principal, interest, and any applicable fees.

What should I do if I have a complaint about Rushmore Servicing?

Start by contacting customer support and clearly explaining the issue. If it is not resolved, submit a written complaint with your loan number, property address, payment details, dates, and supporting documents. Keep copies of everything you send.